The world market for waste incineration plants

By: Maria Kelleher

Solid Waste Magazine 2008-08-01

Waste incineration with energy recovery, referred to as energy from waste (EFW) in Canada and as waste to energy (WTE) in the US and Canada, is looking better economically these days than it has for a long time. The costs of EFW are frequently quoted as around $125/tonne, compared to $50-$70/tonne for landfilling. However, bizarre combinations of high fuel prices, which now make the economics of long haul to landfill less economically attractive, as well as high energy prices, which improve the bottom line for incinerators, are generating interest in new projects for North America for the first time in many years.

Meanwhile, construction of incineration plants, and expansion or refurbishment of existing plants, is on the increase.

A recent study The World Market for Waste Incineration Plants provides details of 800 WTE facilities (1.850 units) in North America, Europe, China and Japan, as well as an assessment of the future for waste incineration in each market.

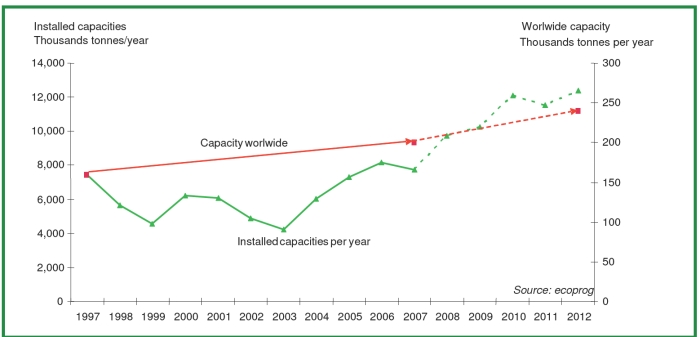

The study concludes that waste incineration is on the increase throughout the world. Global capacity has increased from 160 to 200 million tonnes per year in the last decade and is expected to expand to 240 million tonnes per year in the next five years.

Today there are about 2,500 incineration plants for municipal solid waste throughout the world. About 1,800 of these plants are in Japan. Japan required all communities, regardless of size, to be responsible for their own waste disposal. To achieve economies of scale, incinerators were constructed at capacities larger than was needed. Today, Japan has a multitude of small incineration plants that only operate a few days per month. The incineration technology and the flue gas treatment is out of date. The study concluded that Japan is the only country where there is excess incineration capacity and many of the existing small incineration facilities may actually close in the future because successful waste diversion has reduced the amount of residual waste which needs to be processed.

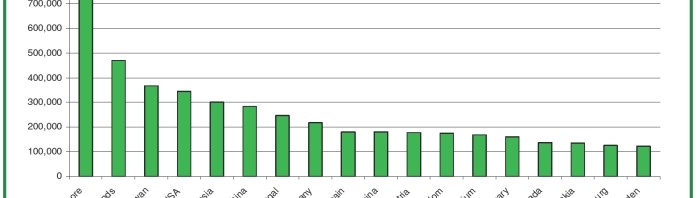

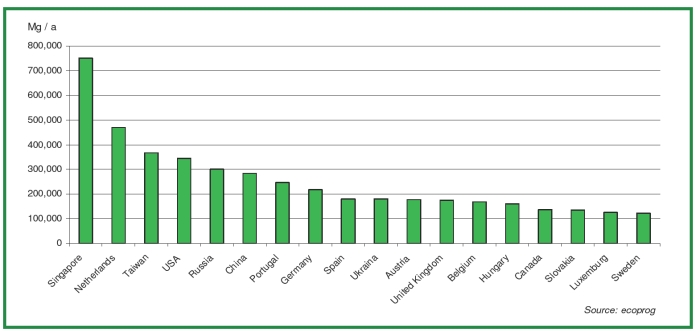

Figure 1 shows the average size of incineration plants by country.

Figure 1 shows the average size of incineration plants by country.

On a worldwide scale China is the country that is currently building the largest number of industrial waste incineration plants. More new plants are planned or under construction in China than in the rest of the world combined. The investment in incineration in China is reported to be 90 euros per tonne of installed annual capacity. That is approximately a sixth of the normal European investment costs of about 540 Euros per tonne of annual operating capacity. When projects are planned in China, tipping fees of 6 euros per tonne are assumed in some cases, compared to at least 90 euros per tonne in Europe.

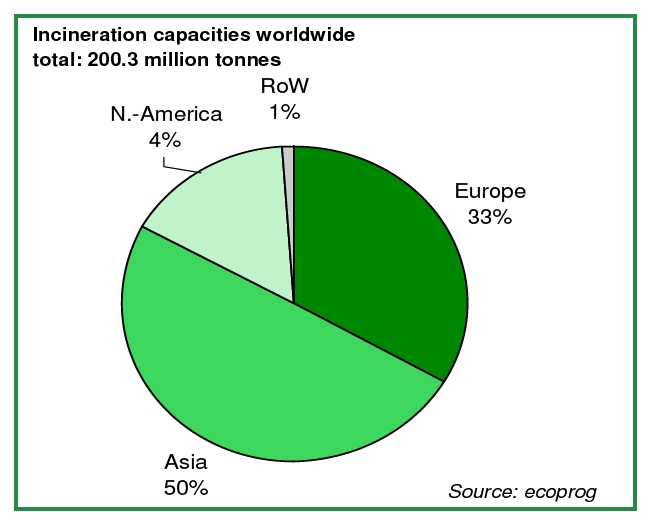

About one third of all incineration capacity globally is in Europe. France has about 130 operating waste incinerators, most of which are old with small capacities. Germany has 80 incineration plants with more than double the French capacities. Denmark. Switzerland and the Netherlands have the highest incineration capacities per capita in Europe.

The trend in installed capacity globally is volatile. The European Union Landfill Directive prohibits the landfilling on unstabilized waste on an increasing scale, expressed as the percentage by which unstabilized waste to landfill must be reduced over time:

- 75 per cent of 1995 level by 2006

- 50 per cent of 1995 level by 2010

- 35 per cent of 1995 level by 2016

Stabilization can be achieved through com- posting, anaerobic digestion or incineration. European countries are constructing numerous MBT (mechanical, biological, thermal) treatment facilities to meet this policy target, but the experience with the MBT technology has been mixed where selling the end products is required to make the facility economically viable. A number of communities are constructing incinerators or RDF (refuse derived fuel) plants to meet the Directive targets. In Europe, the RDF is typically used as a coal substitute in cement plants.

There are 290 incineration projects on the books globally at this time. About 60 of these are in progress, 20 are approved and at least 150 are at the planning stages. An additional 50 are under consideration.

While a slow down is expected in Europe after the current batch of approved incineration plants and expansions are constructed, new facilities are planned in the United Kingdom and Scandinavia, starting in 2011/2012.

The “The Global Market for Waste Incineration Plants”, newly published by ecoprog and Fraunhofer UMSICHT of Germany, examines the market for waste incineration plants and operations around the world. For France and Belgium RDC Environment supported the evaluation. Maria Kelleher and Janet Robins of Kelleher Environmental provided the North American research. The study sells for 4,000 Euros.

For more information, contact Maria Kelleher at mkelleher@kelleherenvironmental.com (416-482-7007, ext 21). More information can be found at www.kelleherenvironmental.com and www.ecoprog.com

Kelleher Environmental is an environmental consulting company based in Toronto which specializes in environmental research, waste management policy, facilitation of environmental processes and climate change.

ecoprog, a Cologne consultancy with offices and representatives in Germany, Canada, Japan, China, France and Italy, specialises in marketing studies for environmental and energy technologies. The Fraunhofer Institute for Environmental, Safety and Energy Technology (UMSICHT) develops, appraises and optimises technical processes relating environmental, safety, process and energy technologies. The two institutions work together to produce market studies on selected sub-segments of the environmental technology market.

Maria Kelleher, P. Eng., is Principal of Kelleher Environmental in Toronto, Ontario. Contact Maria at mkelleher@kelleherenvironmental.com